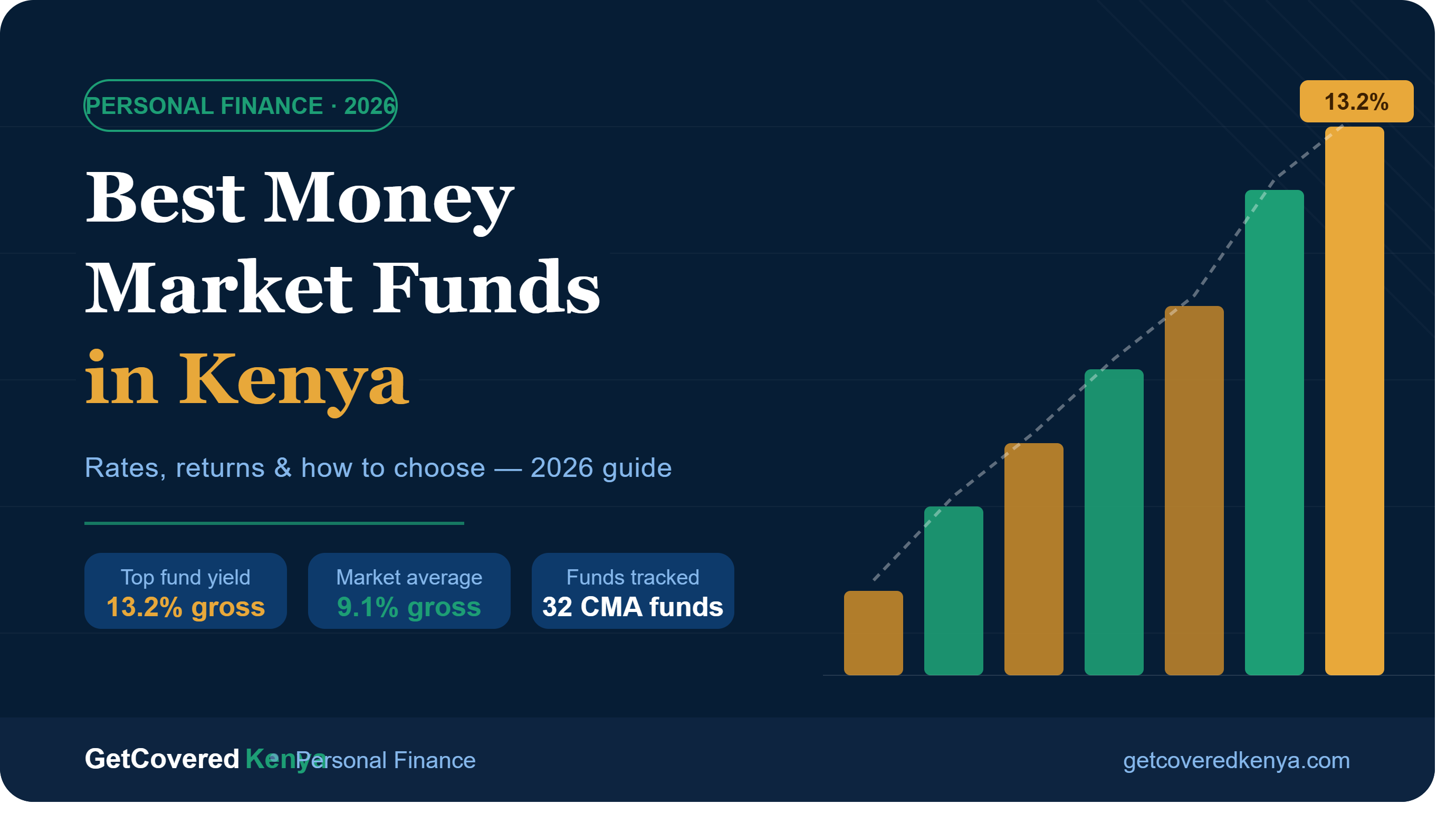

Best Money Market Funds in Kenya 2026 — Rates, Returns & How to Choose

General

Best Money Market Funds in Kenya 2026 — Rates, Returns & How to Choose

- By Brian Ndege

- June 23, 2026

If you are looking for the best money market funds in Kenya right now, you are in the right place. This guide covers every factor that actually matters — current gross and net yields, fund size, fees, minimum investment, liquidity, and how 15% withholding tax affects your real return.

We have pulled live data from the June 2026 industry table tracking all 32 CMA-regulated Kenyan money market funds. By the end of this article, you will know exactly which fund fits your situation — and which ones are quietly losing you money.

What Is a Money Market Fund — and What Makes One the "Best"?

A money market fund (MMF) in Kenya is a CMA-regulated collective investment scheme that pools investors' money into short-term, low-risk assets — primarily Treasury Bills, bank fixed deposits, and high-grade commercial paper.

The "best" MMF balances a competitive net yield (above Kenya's 6.7% inflation rate), strong liquidity, a proven track record, manageable fees, and a low minimum investment. There is no single best fund for every investor.

Why Are Kenyans Flocking to Money Market Funds in 2026?

The numbers tell the story clearly.

A standard bank savings account in Kenya pays between 1% and 4% per year. The industry average money market fund interest rate as of June 2026 sits at 9.1% gross — or roughly 7.7% net after the mandatory 15% withholding tax deducted by KRA.

That is more than double what most savings accounts pay, for the same level of accessibility and a comparably low risk profile.

Three factors are driving the surge in money market fund uptake among Kenyan retail investors in 2026:

- M-Pesa integration. Most funds now accept deposits and process withdrawals directly via M-Pesa, removing every barrier to entry.

- Low minimums. Several top-rated funds accept starting investments of KES 100 to KES 1,000 — making them genuinely accessible to first-time investors.

- Daily compounding. Interest accrues every single day on most Kenyan MMFs, meaning your money starts earning from day one and compounds continuously.

The Capital Markets Authority (CMA) of Kenya regulates all money market funds under the Capital Markets Act. Every fund in this article is CMA-licensed, giving investors the assurance of regulatory oversight and mandatory daily yield disclosure.

What Are the Current Money Market Fund Interest Rates in Kenya?

This is the question every investor asks first — and it deserves an honest, data-backed answer.

As of the industry table published for the week of 19 June 2026, the Kenyan money market fund landscape looks like this:

- Highest yielding fund: Nabo Africa — 13.2% gross EAR

- Industry average: 9.1% gross (approximately 7.7% net after 15% WHT)

- Lowest yielding fund: Equity Money Market Fund — 5.1% gross (below Kenya's 6.7% inflation rate)

- Total funds tracked: 32 CMA-regulated KES money market funds

- Spread between best and worst: 8.1 percentage points

That spread matters enormously. On KES 500,000 invested for one year, the difference between the best-performing fund (13.2%) and the worst (5.1%) is approximately KES 38,500 in additional interest. That is not a rounding error — it is real money.

Critical note on reading yields: Every headline rate you see quoted for a Kenyan money market fund is the gross effective annual rate (EAR) — before the 15% withholding tax. To calculate your actual net return, multiply the gross rate by 0.85. A fund yielding 12% gross pays you approximately 10.2% net. Always compare funds on a net-of-tax basis.

How Does the 15% Withholding Tax Affect Your Money Market Fund Return?

Understanding the money market fund interest rate tax treatment in Kenya is non-negotiable before you invest.

Under Section 35 of the Kenya Income Tax Act, all interest income earned from money market funds is subject to a 15% withholding tax (WHT), deducted at source by the fund manager before your interest is credited. You receive the net amount automatically — no filing or declaration is required for individual investors.

Here is how the tax plays out in real numbers:

| Gross Rate | WHT (15%) | Net Rate | Return on KES 100,000/year |

|---|---|---|---|

| 5.1% (Equity — lowest) | 0.77% | 4.3% | KES 4,300 |

| 6.7% (inflation rate) | 1.0% | 5.7% | KES 5,700 |

| 8.4% (CIC) | 1.26% | 7.1% | KES 7,100 |

| 9.1% (industry avg) | 1.37% | 7.7% | KES 7,700 |

| 9.2% (Sanlam) | 1.38% | 7.8% | KES 7,800 |

| 11.4% (Cytonn — May 2026) | 1.71% | 9.7% | KES 9,700 |

| 13.2% (Nabo — June 2026) | 1.98% | 11.2% | KES 11,200 |

The tax applies only to interest earned — never to your principal. Switching funds does not trigger any additional tax event. You pay WHT on interest, and that is the end of your tax obligation.

The Best Money Market Funds in Kenya — June 2026 Comparison Table

The table below compares the leading CMA-regulated Kenyan money market funds across the criteria that actually determine value: yield, fund size (AUM), management fee, minimum investment, and liquidity speed.

Data sources: Business Daily Kenya industry table (week of 19 June 2026); individual fund manager fact sheets (May–June 2026); Capital Markets Authority fund registry. Rates are gross effective annual yields and change weekly with the CBK policy rate cycle. Always verify current rates directly with the fund manager before investing.

| Fund | Gross EAR (June 2026) | Net EAR (after 15% WHT) | Min. Investment | Mgmt Fee | AUM | Liquidity |

|---|---|---|---|---|---|---|

| Nabo Africa MMF | 13.2% | ~11.2% | KES 1,000 | ~1.5% | Medium | 3–5 days |

| Cytonn MMF | ~11.4–11.9% | ~9.7–10.1% | KES 100 | ~2.0% | Medium | 3–5 days |

| Arvocap MMF | ~11.8–12.1% | ~10.0–10.3% | KES 1,000 | ~1.5% | Smaller | 3–5 days |

| Etica MMF | ~11.2% | ~9.5% | KES 1,000 | ~1.5% | Smaller | 3–5 days |

| Lofty-Corban MMF | ~10.7% | ~9.1% | KES 5,000 | ~1.5% | Growing | 3–5 days |

| Britam MMF | ~9.4–10.0% | ~8.0–8.5% | KES 1,000 | ~2.0% | Large | T+1–3 days |

| SanlamAllianz MMF | ~9.1–9.2% | ~7.7–7.8% | KES 2,500 | 2.0% | KES 127B | 2–4 days |

| CIC MMF | ~8.4% | ~7.1% | KES 5,000 | ~2.0% | Large | 2–4 days |

| NCBA MMF | ~8–9% | ~6.8–7.7% | KES 1,000 | ~1.5% | Large | T+1 |

| Old Mutual MMF | ~8–9% | ~6.8–7.7% | KES 1,000 | ~2.0% | Large | 2–3 days |

| Stanbic MMF | ~5.3% | ~4.5% | KES 5,000 | ~1.5% | Large | T+1 |

| Equity MMF | ~5.1% | ~4.3% | KES 1,000 | ~1.5% | Large | T+1 |

| Ziidi (Sanlam/M-Pesa) | ~6.1% | ~5.2% | KES 100 | ~1.5% | Large | Same day |

AUM = Assets Under Management. T+1 = funds credited within one business day of redemption request.

How to Choose the Best Money Market Fund for Your Situation

Is the Highest Money Market Fund Interest Rate Always the Right Choice?

No. And this is the most important thing this article can tell you.

The fund paying 13.2% this week may not be paying 13.2% next month. Money market mutual fund interest rates in Kenya move every single week, tracking the Central Bank Rate (currently 8.75%) and the weekly 91-day Treasury Bill rate. The June 2026 industry table shows rates ranging from 5.1% to 13.2% — an 8.1-point spread. That ranking shifts constantly.

Chasing the weekly rate leader is a strategy that sounds logical and performs poorly in practice.

The better question to ask is: which fund consistently delivers a competitive net yield from a stable, well-run platform with reliable liquidity?

Here are the five criteria that should drive your decision.

Criterion 1: Does the Fund Beat Inflation?

Kenya's inflation rate stood at 6.7% for the year to May 2026 (Kenya National Bureau of Statistics). Any money market fund paying below 6.7% gross is shrinking your real spending power, not growing it.

Four funds in the June 2026 industry table are currently below the inflation line:

- Equity MMF — 5.1% gross

- Stanbic MMF — 5.3% gross

- AA Kenya Shillings — 6.0% gross

- Ziidi — 6.1% gross

These funds are not unsafe. They are CMA-regulated and your principal is not at unusual risk. But on a real returns basis, holding money in them means your KES buys less each year. This is the first filter every Kenyan investor should apply.

Criterion 2: Fund Size and Track Record

A fund's Assets Under Management (AUM) is a proxy for investor trust and operational stability.

Kenya's largest money market fund is the SanlamAllianz Money Market Fund, with a KES 127 billion portfolio as of the May 2026 fact sheet. Its portfolio composition — 57% cash and bank deposits, 38% Treasury securities, 5% corporate debt — reflects the conservative allocation that characterises a well-run large fund.

Large fund size matters for two practical reasons:

- Redemption stability. Large funds handle simultaneous withdrawal requests from many investors without needing to liquidate assets at unfavourable prices.

- Track record. Sanlam's fund has operated since November 2014. Cytonn has been a consistent top-tier performer across multiple CBK rate cycles. A fund with a ten-year track record through Kenya's interest rate fluctuations tells you something a new entrant cannot.

Newer or smaller funds — including some of the current top-rate performers — may not have been tested through a prolonged rate downturn. That does not make them bad investments, but it is a genuine risk factor that a raw yield comparison does not capture.

Criterion 3: Management Fee — the Silent Return Killer

Most Kenyan money market funds charge an annual management fee of between 1.5% and 2.5% of your invested balance. This fee is deducted before the fund publishes its yield — meaning the rate you see in the industry table is already after the management fee has been taken.

But fees matter when comparing funds that appear similar on yield.

A fund at 9.5% gross with a 1.5% fee is structurally different from a fund at 9.5% gross with a 2.5% fee — even though both publish the same yield. The higher-fee fund needs to generate significantly better gross investment returns just to show you the same number. When rates compress — which happens in a falling CBK rate environment — the high-fee fund feels the squeeze faster.

Always ask for the management fee, and always think about it as a structural headwind to long-term performance.

Criterion 4: Liquidity — How Quickly Can You Access Your Money?

A money market account is not a fixed deposit. You should be able to access your money when you need it. But "accessible" means different things across different Kenyan MMFs.

- T+1 liquidity (funds credited within one business day): Offered by NCBA, Old Mutual, Stanbic, and Equity — typically bank-backed funds with direct payment infrastructure.

- 2–4 business days: The standard for most large CMA-regulated funds including Sanlam and CIC.

- 3–5 business days: Common among boutique and specialist fund managers, including several of the higher-yielding options.

- Same-day: Ziidi (via M-Pesa) offers the fastest access in the market — but at 6.1%, it pays below inflation.

For an emergency fund — money you might need without warning — faster liquidity is worth a meaningful yield sacrifice. For medium-term savings goals where you will not need sudden access, a 3–5 day redemption window is entirely acceptable.

Criterion 5: Minimum Investment and Access Method

The good money market funds in Kenya have dramatically lowered their entry barriers:

- KES 100 minimum: Cytonn, Ziidi

- KES 1,000 minimum: Nabo Africa, Etica, Arvocap, Britam, Old Mutual, NCBA

- KES 2,500 minimum: SanlamAllianz

- KES 5,000 minimum: CIC, Lofty-Corban, Stanbic

All top-rated money market funds in Kenya accept M-Pesa deposits. Most also offer USSD access (# codes) for investors without smartphones. This accessibility is a genuine structural advantage Kenya's MMF market has over many comparable markets globally.

How to Invest in Money Market Funds in Kenya — Step by Step

Investing in a Kenyan money market fund takes less than 15 minutes if you have your documents ready. Here is the exact process.

- Choose your fund. Use the comparison table above to identify funds that beat inflation, have a track record you trust, and offer the liquidity speed your situation requires.

- Gather your documents. You need your National ID or passport number, your KRA PIN (available from KRA's iTax portal), and your M-Pesa-registered phone number. No physical paperwork or medical examination is required.

- Register online. Visit the fund manager's website or download their app. Complete the online KYC (Know Your Customer) form with your personal details, ID number, and KRA PIN. Most registrations are approved within minutes during business hours.

- Fund your account via M-Pesa. Once registered, you will receive an M-Pesa paybill number or account number. Send your initial deposit from M-Pesa. Most funds confirm receipt within minutes and begin crediting interest from that same day.

- Set up a standing order (optional but recommended). The most effective strategy for building wealth in a money market fund is regular monthly top-ups via M-Pesa standing order. Even KES 2,000 per month at 9% over 10 years compounds into a meaningful sum.

- Monitor your account. Log in to your fund's portal or app monthly to confirm your balance, accrued interest, and the current yield. Check the live industry rate table periodically to ensure your fund remains competitive.

- Redeem when needed. Submit a redemption request through the fund's app or website. Your money arrives in your M-Pesa or bank account within the fund's stated liquidity window.

USD Money Market Funds in Kenya — What You Need to Know

The dollar money market fund is an increasingly popular option for Kenyan investors with USD earnings, diaspora remittances, or a desire to hold savings in a hard currency.

As of June 2026, the USD money market fund landscape in Kenya shows:

- Highest yielding USD MMF: Nabo Africa USD — 7.14% gross EAR

- Industry average (USD): approximately 5.0% gross EAR

- WHT: 15% applies to USD MMF interest income, identical to KES funds

USD MMFs in Kenya invest primarily in US Treasury Bills, international bank deposits, and short-term US-dollar-denominated commercial paper. They offer:

- Protection against Kenya Shilling depreciation

- Lower yields than KES funds (reflecting lower US interest rates vs. Kenyan rates)

- The same CMA regulatory framework as KES funds

Who should consider a USD money market fund?

- Kenyans with dollar-denominated income — exporters, diaspora remittance recipients, or those paid in USD

- Investors who want to hold reserves in a hard currency without the volatility of equity markets

- Businesses with dollar payables in the near term that need to park USD safely and earn a return

Who should stick to KES funds?

- Investors with KES-denominated expenses and financial goals — which describes most Kenyan retail investors

- Anyone whose primary risk is local inflation, not currency depreciation

The KES-USD spread is significant. Kenya's best KES fund currently yields 13.2% gross against the best USD fund at 7.14% gross. For KES-based investors, local currency funds almost always win on headline yield — but that comparison ignores the depreciation risk in the shilling. Choosing between KES and USD funds is ultimately a currency and risk question, not just a yield question.

Money Market Funds vs. Other Kenyan Investment Options

How does investing in money market funds compare to the other savings and investment vehicles available to Kenyan investors?

| Investment Vehicle | Typical Annual Return | Liquidity | Risk Level | Min. Investment | Regulated By |

|---|---|---|---|---|---|

| Bank savings account | 1–4% | Instant | Very low | KES 0 | CBK |

| Money market fund (KES) | 5.1–13.2% gross | 1–5 days | Very low | KES 100–5,000 | CMA |

| Treasury Bills (91-day) | ~9–10% | Lock-in (91 days) | Negligible | KES 100,000 | CBK |

| Treasury Bonds | 13–16% YTM | Lock-in (1–25 yrs) | Very low | KES 50,000 | CBK |

| Fixed Deposits (banks) | 7–12% | Lock-in (1–12 months) | Very low | KES 50,000+ | CBK |

| SACCO deposits | 10–13% (dividends) | Annual | Low | Varies | SASRA |

| USD MMF | 5.0–7.1% gross | 1–5 days | Very low | USD 100–1,000 | CMA |

| NSE equities | Variable (-30% to +40%) | 3 days (T+3) | High | KES 1,000 | CMA |

The money market fund occupies a unique position: it offers returns significantly above a savings account with nearly identical liquidity, while carrying far lower risk and a much lower minimum investment than Treasury Bills or fixed deposits.

For the emergency fund portion of any investor's portfolio — the 3–6 months of living expenses that must remain accessible at all times — a top-rated Kenyan money market fund is the most rational home for that capital.

What Is a Money Market Deposit Account — and Is It the Same as an MMF?

Many investors confuse a money market deposit account (MMDA) with a money market fund, and it is worth clarifying the distinction.

A money market deposit account is a bank product, not a CMA-regulated investment fund. In the Kenyan context, MMDAs are interest-bearing call accounts offered by commercial banks — similar to high-yield savings accounts. They are regulated by the Central Bank of Kenya (CBK) rather than the CMA.

Key differences:

- MMDAs offer lower rates (typically 3–7%) but carry implicit bank deposit protection

- Money market funds are not deposits — they are units in a collective investment scheme; your "balance" is expressed in units, not KES directly

- MMFs are regulated by the CMA and governed by the Collective Investment Schemes Regulations

- MMDAs count against CBK deposit insurance limits; MMFs do not — making fund diversification a consideration for large investors

For most Kenyan retail investors, the practical implication is straightforward: a CMA-regulated money market fund almost always offers a superior yield compared to a bank's money market deposit account, with comparable safety and similar (or better) liquidity.

The Kenyan MMF Market in 2026 — Macro Context and Rate Outlook

Understanding why money market fund interest rates are where they are in 2026 helps you make better investment decisions.

The Central Bank of Kenya (CBK) cut its policy rate from 9.0% in January 2026 to 8.75% in February 2026. That single decision is the primary driver of the gradual decline in MMF yields from the 2025 peaks — when several funds were paying above 14% gross.

The 91-day Treasury Bill rate — the benchmark that most Kenyan MMFs are benchmarked against — has trended downward alongside the CBK rate. As of the bill issued 22 June 2026, the T-Bill yield sits below the industry average MMF rate of 9.1%, which means the best funds are generating slightly above the benchmark they hold. That outperformance is a positive signal.

Kenya's inflation rate was 6.7% in May 2026 (KNBS), with food inflation at 9.4% and transport at 16.5%. The CBK's Monetary Policy Committee (MPC) meeting on 11 June 2026 was closely watched. If inflation remains elevated above 6%, the CBK is expected to hold or tighten — which would be positive for MMF yields as T-Bill rates stabilise or rise.

The key takeaway for investors: the exceptional 14–15% gross yields of 2024–2025 are unlikely to return in the short term. The current 9–13% range for top funds, while lower than recent peaks, still represents genuinely strong real returns for a low-risk, liquid asset. An average Kenyan money market fund paying 9.1% gross against 6.7% inflation delivers a real return of approximately 2.4% — positive, meaningful, and far superior to any bank savings account.

Common Mistakes Kenyan Investors Make With Money Market Funds

Mistake 1: Staying in a Fund That Loses to Inflation

Four of the 32 Kenyan MMFs tracked in the June 2026 industry table pay below Kenya's 6.7% inflation rate. Millions of Kenyans hold money in the Equity MMF (5.1%), Stanbic MMF (5.3%), AA Kenya Shillings (6.0%), and Ziidi (6.1%) — partly because the fund was one tap away inside an app they already used.

Switching funds carries no penalty, no lock-in, and no tax event. Moving from a below-inflation fund to the industry average (9.1%) adds approximately KES 20,000 per year on KES 500,000 invested — for zero additional risk.

Mistake 2: Choosing a Fund Based on Last Month's Rate

Rates change weekly. The fund topping the table in May may be fourth by July. Choosing a fund purely based on its position in one week's industry table means you are making a long-term decision on a short-term data point.

Choose based on sustained performance, fund size, fee structure, and liquidity — then verify the current rate is at or above the market average.

Mistake 3: Ignoring the Management Fee

Two funds can quote the same gross yield while delivering meaningfully different net returns after fees. Always ask for the annual management fee and check whether the published yield is before or after it has been deducted. In Kenya, the published EAR is typically after management fees — but always confirm.

Mistake 4: Treating an MMF as a Long-Term Investment Substitute

Money market mutual funds are excellent vehicles for short to medium-term cash management — emergency funds, saving for a specific goal within 1–3 years, or parking cash between investment decisions. They are not optimised for long-term wealth building compared to equities, bonds, or real assets over a 10–20 year horizon.

A sound personal finance strategy uses an MMF for its liquidity and stability, while deploying longer-term capital into higher-returning assets appropriate to your risk tolerance and time horizon.

Mistake 5: Not Protecting the Income That Feeds Your MMF

This is a risk that almost no money market fund guide mentions — because it is not a fund selection question. It is a financial planning question.

Your ability to make regular monthly contributions to a money market account depends entirely on your income continuing. A medical emergency that sidelines you for three months, a disability that prevents you from working, or a family breadwinner's death can stop those contributions permanently.

The Kenyan investors who build the most wealth through compound interest are not just the ones who choose the best fund — they are the ones who protect their ability to keep contributing. That means life insurance to protect your dependants, personal accident cover to replace lost income after injury, and health insurance to prevent medical bills from draining the account you spent years building.

Compound interest works by staying uninterrupted. Protecting your income is how you keep it that way.

Frequently Asked Questions — Best Money Market Funds Kenya

What is the best money market fund in Kenya right now?

As of the industry table published 19 June 2026, Nabo Africa leads at 13.2% gross EAR. However, "best" depends on your priorities. For pure yield, Nabo, Cytonn, and Arvocap are the top tier. For size, track record, and liquidity combined, SanlamAllianz (KES 127 billion AUM, 11-year track record, 9.2% gross) is the most widely recommended default for most Kenyan savers. Always verify current rates before investing — the table changes weekly.

How much do I need to invest in a money market fund in Kenya?

Minimum investments range from KES 100 (Cytonn, Ziidi) to KES 5,000 (CIC, Stanbic). Most top-rated money market funds in Kenya start at KES 1,000. There is no practical financial reason to wait until you have a large lump sum — the power of compound interest rewards starting early with whatever you have.

How is money market fund interest taxed in Kenya?

All MMF interest income is subject to a 15% withholding tax (WHT) under the Kenya Income Tax Act, Section 35. The fund manager deducts and remits this to KRA automatically — you receive the net amount credited to your account and have no further filing obligation as an individual investor. The tax applies only to interest earned, never to your principal balance.

Are money market funds safe in Kenya?

All CMA-regulated money market funds in Kenya are considered very low risk. They invest primarily in government-backed securities (Treasury Bills), bank deposits with regulated commercial banks, and high-grade corporate paper. Your principal is not capital-guaranteed in the technical sense — they are not bank deposits — but the asset quality requirements imposed by the Capital Markets Authority mean that principal loss is an extremely remote risk for a well-run, compliant fund. The primary risk is yield risk — rates going up or down with the CBK cycle — not capital loss.

What is the difference between a money market fund and a money market account?

In Kenya, a money market fund (MMF) is a CMA-regulated collective investment scheme. A money market account or deposit account (MMDA) is a CBK-regulated bank product. MMFs generally offer significantly higher yields (9–13% vs 3–7%), slightly less instantaneous liquidity (1–5 days vs instant), and are not covered by bank deposit insurance. For most retail investors seeking a balance of return and accessibility, a CMA-regulated MMF is the better option.

Can I invest in a USD money market fund from Kenya?

Yes. Several Kenyan fund managers offer USD-denominated money market funds, with the leading fund (Nabo Africa USD) paying 7.14% gross EAR as of June 2026. USD funds are appropriate for investors with dollar income or those seeking currency diversification. They carry the same 15% WHT on interest and are regulated by the CMA. USD fund yields are lower than KES funds, reflecting the global interest rate environment.

Conclusion — Choosing the Best Money Market Fund for You

The best money market funds in Kenya in 2026 are not simply the ones paying the highest rate this week.

The best fund for you is the one that consistently beats inflation (above 6.7% gross), operates within a large, stable, CMA-regulated framework, charges reasonable fees, delivers reliable liquidity when you need it, and is easy to use via M-Pesa so you can keep contributing every month without friction.

For most Kenyan retail investors, that points toward the mid-to-large tier of the market: Sanlam, CIC, Britam, NCBA, and Old Mutual for stability and size; Cytonn, Nabo Africa, Etica, and Arvocap for investors willing to accept smaller fund size in exchange for meaningfully higher yields.

What to avoid is equally clear: funds paying below Kenya's 6.7% inflation rate — currently Equity, Stanbic, Ziidi, and AA Kenya Shillings — regardless of how convenient the app or how trusted the parent brand.

Start today. Start with what you have. Pick a fund that beats inflation. Contribute monthly. Protect the income that makes those contributions possible. Let compound interest do the rest.

QA Blueprint — FAQ

Question 1: Q: What is the best money market fund in Kenya in 2026? A: As of 19 June 2026, Nabo Africa leads the 32-fund industry table at 13.2% gross effective annual yield. For investors prioritising size and stability over peak yield, SanlamAllianz — Kenya's largest MMF at KES 127 billion AUM — is the most widely recommended default, paying 9.2% gross (approximately 7.8% net after 15% withholding tax).

Question 2: Q: How do I invest in a money market fund in Kenya via M-Pesa? A: Step 1: Choose a CMA-regulated fund using the industry rate table. Step 2: Gather your National ID number and KRA PIN. Step 3: Register online at the fund manager's website or app. Step 4: Fund your account by sending money to the fund's M-Pesa paybill number. Step 5: Interest begins accruing from the day of deposit. Redemptions are processed within 1–5 business days depending on the fund.

Question 3: Q: What is the money market fund interest rate in Kenya right now? A: As of the week of 19 June 2026, the Kenyan money market fund industry average is 9.1% gross effective annual yield. The highest rate is 13.2% gross (Nabo Africa) and the lowest is 5.1% gross (Equity MMF). All rates are subject to 15% withholding tax — multiply the gross rate by 0.85 to get your actual net return.

Question 4: Q: Are money market funds safe in Kenya? A: Yes, with appropriate qualification. All CMA-regulated Kenyan money market funds are very low risk — they invest primarily in Treasury Bills, regulated bank deposits, and high-grade commercial paper. Your principal is not capital-guaranteed (they are not bank deposits), but principal loss is an extremely remote risk for a compliant, well-run fund. The primary risk is yield fluctuation, not capital loss. Verify any fund's CMA licence at cma.or.ke before investing.